They’re only 16 feet above sea level, they already have issues with salt water incursion into the freshwater supply, and there’s a Superfund site 750 feet away from the water supply for all of Miami.

And I wasn’t joking about the storm surge either. Tampa is 80 feet above sea level, Miami averages 16.

The only advantage of Miami is that the mayor of Miami has explicitly said “Fuck those Commies who ruined SF”.

/There’s some personal reasons for this as well, but I really don’t want to have to move to Miami.

I respect you and your weird outlooks and choices but “Let’s all the rich people go move somewhere teetering on the brink of absolute infrastructure catastrophe where the mayor PROMISES not to tax anybody” has possibly the highest entertainment value yet

I know right!

This was 1992, when FL’s population was 2/3rds what it is now.

The South is a couple of strategic ports, a series of *inland* cities because hurricanes… and Florida, 20 Million people sitting out on a stick. It’s already a 2-day drive to evacuate from Tampa to the state border when a hurricane hits. Everyone who moves there is crazy, but all the people who want to employ me are *moving there*.

Aren’t a bunch of tech companies moving to Austin? I’ve certainly heard more mumbling about Austin than Miami on twitter, but maybe that’s just my bubble.

I know everybody thinks us tech workers are rootless, atomized yuppies who are only in San Francisco etc. because that’s where the jobs are, but I actually like Seattle, and I know plenty of people who feel the same way about the Bay Area (housing costs aside).

(That said, everyone else should take OP’s advice and move to Miami so I can get a cheaper condo here)

I mean, I liked NYC before my knee blew out and I was no longer capable of standing on moving trains right as the local Armenians started having nightly gunfights and my entire industry evacced the dying, collapsing, suddenly crime-ridden city.

/NYC used to have a crime rate less than the national average.

In the year of our Lord 2021, a material-enough-to-have-to-upend-your-life-for percentage of tech/finance companies are *still* planning to make you live in the same state as them if you want to work for them? That’s fucked up.

(My dad worked tech in San Francisco for a while, but that didn’t mean he *lived* there, *god* no. He lived in *Canada* like a *sensible* person.)

((no offense to my friends in San Francisco, I assume you’re making the best of a bad situation))

—

I mean, I guess if you’re used to California even Miami might seem like an improvement danger-wise? Like, on a scale of 1 to California, Miami is what, a 9?

“Arranging for rich people to live in incredibly disaster-prone environments” doesn’t sound like an anti-communist position at all. That’s just using hurricanes/earthquakes/wildfires instead of guillotines.

Tags:

#getting an IFRS-based accounting designation is increasingly seeming #like a kind of precommitment against the San Francisco Gravitational Field and its descendants #”nope‚ my credentials don’t transfer to the States‚ you’ll just have to go on without me‚ so sorry‚ byeeee” #(renouncing my U.S. citizenship would be an even stronger oath to never move there but I’m still not sure if I’m willing to go *that* far) #((a few years back my dad refused a job offer from Google that was conditional on moving to SF)) #((better to work at Uber Eats here than to work at Google there)) #(((well at the time it was ”better to be unemployed” etc: Uber Eats came later))) #on a scale of 1 to California my area is maybe a 2 #there’s occasional ice storms you have to watch out for and that’s basically it #(*knocks on wood*) #home of the brave #our home and cherished land #adventures in human capitalism #101 Uses for Infrastructureless Computers #reply via reblog #apocalypse cw #death tw? #murder cw?

I wrote this as a tag ramble because it felt like a tag-register kind of post, but I’m running out of space in the tag box and also I don’t want to discourage people from responding to me (apparently a lot of people interpret tag rambles as followers-only posts? and it’s certainly more effort to quote them, in any case), so here it is:

#the great thing about living with your parents is that it gives you potentially as much as two or three decades to figure out #where the fuck you’re going to find platonic nesting partners after they’re dead #(the other great thing is that you don’t have to spend years trying desperately to make your savings outpace the rise in house prices) #(because you can just take over your dad’s HELOC) #(but that’s *somewhat* tangential to this post) #I guess I could *try* living alone for a while but I don’t think I’d like it #I could probably *tolerate* it and there’d be *some* upsides #but yeah it *is* very inefficient #and it seems like it would be rather lonely and frankly kind of dangerous #(I have this suspicion that a lot of the lifespan benefits of marriage are simply from having a housemate) #(someone to take care of you (and also of basic household maintenance) when you’re sick) #(someone to hear you choking) #(someone to find you passed out on the floor) #(someone to hug you in lockdowns so you don’t break down from touch deprivation) #one-breadwinner households were a historical aberration and their time has ended #it’s time to spruce up the homestead system to make it less dependent on having [living family] [that you like being around] #(okay I went and looked up homesteading and maybe that’s not *quite* the right word) #(I think it’s just that most of the family-sized communes I know of #–that *weren’t* forged in the extreme pressures of San Francisco†– #are homesteads) #((I mean *ideally* it’d be good to have enough skillsets and executive function and physical function and land between us that #we *could* retreat into self-sufficiency in a crisis)) #((but “division of labour is good” extends beyond the household level)) #†I really don’t want to live in San Francisco‚ please don’t make me move to San Francisco just to find a commune

Tags:

#tag rambles #reply via reblog #death tw #adventures in human capitalism #illness mention

I have been feeling increasing anxiety about AI given the success of gpt-3, and not because of the potential of a singularity or AI foom scenario.

What I’m worried about is that AI will soon make nerds obsolete. In the current world, you can be socially awkward and weird but still find success and status through your intellectual abilities. There are many jobs available for people who can write, code, or even just memorize a lot of information (like lawyers). But it seems like we may not be too far off from AI being able to take many of these jobs over. Perhaps not the most complicated and high status ones, but the bulk of the low and mid-range complexity jobs that most nerds work in will disappear.

If AI takes over most of these information jobs, then what’s left will be physical labor and people-oriented jobs. Everyone will be either a construction worker or yoga instructor. The salespeople will be fine, meanwhile most data analysts and entry level coders and writers will be laid off as one person plus an AI can do the work of dozens of people.

Right now, you can still get some level of societal respect if you’re smart even if you lack charisma or physical ability, but that may not be true much longer.

…both physical labor and, uh, let’s call it “user interface labor” are already getting hammered by automation. That doesn’t seem likely to stop or slow down.

(A high-level salesperson dealing with high-value wares may not be replaceable by present-generation AI…GPT-3 can’t schmooze a client…but the McDonald’s cashier is getting replaced by a kiosk, and the ordinary floor salesman is getting replaced by the Amazon algorithm.)

It is true that intellectual labor may be thrown into that basket as well.

Social respect stems from economically productive labor is a mug’s game. We’ve been falling down on the job of dealing with that truth, in part because nerds – who are, de facto, responsible for that kind of philosophical work – have been doing very well economically of late. But it remains true.

The lucrative remuneration for analytical thinking of the past couple decades should be understood as a blip. Eventually it will die down, and that will suck for many people (including myself.) But you shouldn’t build your life counting on it to last.

Save the money you earn now instead of counting on a regular increase in pay throughout the rest of your life. Talk to lawyers you know about what their professional arc has looked like (given that they have had the same arc recently.) Vote for a strong social safety net because even if you earn 6 figures now you may need it later.

I don’t really have good advice for people. A lot of people are in very bad situations! But “I and my friends have well paying jobs and I expect this to never change” is not guaranteed to hold up.

+1

I’m going into accounting soon, and I plan to operate under the assumption that I will be permanently laid off at some point. Here’s hoping it’s far enough in the future to give me a good chance to prepare.

(On the bright side, my *baseline* expenses are barista FIRE†, and I have several Vimes Boot Theory plans that I would only need a few good years to be able to enact. Also I have my foot in the employees-only door at a local fast-food joint, which is in a small town where automation of fast food is less economical.)

I won’t make the same mistakes my father made, thinking that because he was a programmer†† he was golden and didn’t need to do more than basic 401k deposits. (I’m gonna make *new* and *different* mistakes, which will almost certainly revolve around having less fun than I could be getting away with having. I’m pretty okay with that.)

—

†”barista FIRE” = the ability to cover your personal expenses on 20 minimum-wage-hours a week (the shortfall is implied to be covered by interest on your investments, but I would *have* no shortfall on 20 minimum-wage-hours/week, though it’d be a bit tight and I wouldn’t be able to support anyone else) ((okay, the lack-of-other-income is not quite true, ~half our rent is being covered by partial ownership of our home and absence-of-rent-cost-due-to-ownership is a form of interest income in its own right; upon reflection, people who come from subcultures where car leasing/loans are normalised would likely also be inclined to consider the absence of payments on our (admittedly shitty) car as a form of interest income))

††of devices that no longer exist, having been subsumed by Blackberries and then even further subsumed by smartphones

Tags:

#reply via reblog #adventures in human capitalism #in which Brin has a job #this probably deserves some warning tag but I am not sure what #apocalypse cw?

On GoodRx, a month’s worth of sildenafil 20 mg costs $17.25

On the same site, a month’s worth of sildenafil 25 mg costs $507.24

Does anyone buy the 25 mg version? You bet – I saw a patient who was on it yesterday (don’t worry; he’s since been switched over).

What’s going on here? Sildenafil has two FDA approvals – one, under the name “Revatio”, for hypertension. The other, under the name “Viagra”, for – well, you know.

The FDA only approved Revatio at doses of 5 and 20 mg, and only approved Viagra at doses of 25 and 100 mg. So sildenafil 20 mg has “Revatio” on the box and sildenafil 25 mg has “Viagra” on the box. Revatio is generic and dirt-cheap; Viagra is still on-patent and expensive.

But can’t people who want Viagra just buy Revatio?

Yes, totally. But the average patient doesn’t know this is going on. And the average doctor doesn’t really have any incentive to care because they’re not the one buying it (I’ve had patients who have asked their doctor to prescribe the cheaper version, and the doctor has refused because they want to do it the “proper” way). And I think it’s illegal for the insurance companies to insist, because technically the FDA only approved sildenafil 25 mg for erectile dysfunction but didn’t approve sildenafil 20 mg.

(also, some people are like “But I need a higher 50 mg dose of Viagra, and Revatio only goes up to 20 mg!” As the ancient rationalist proverb goes, have you tried thinking about the problem for five minutes?)

At the advice of my doctor, I’m on pseudo-prescription naproxen. Instead of one 500mg prescription pill, I buy the 220mg OTC stuff and take double the dose on the label: it’s close enough, and it’s somewhat cheaper per mg if you don’t have prescription coverage. She said if I ever do get prescription coverage I should let her know and she’ll write me an official prescription then.

I love my doctor.

—

(Please do not take prescription-strength naproxen without medical supervision: you can fuck up your liver.)

—

Side benefit:

People in the spring: “it’s horrible that they’re making *chronically ill* people go to a *pharmacy* *every month* and risk plague! patients aren’t allowed to keep buffers of medications they often need to *survive*!”

Me: *looks with a mixture of relief and awkwardness at my 200-pack of Aleve*

(Note: I only need it around the onset of menstruation, so 200 OTC-sized pills is about a ten-month supply.)

(Store-brand naproxen doesn’t come in 200-pack, and the bulk-discount benefit outweighed the name-brand penalty.)

Tags:

#other things my doctor has done: #prescribed prune juice for constipation #prescribed string for skin tags #used Big Pharma ”samples” to keep her poorer patients supplied with meds they would struggle to afford on their own #readily admitted that people in my situation don’t actually need gynecological checkups #and I should only see a gynecologist if something goes wrong or I decide to start having sex #reply via reblog #adventures in human capitalism #medical cw #illness mention #covid19 #menstruation #this probably deserves some other warning tag but I am not sure what

so like. there’s this budgeting thing called the 50/30/20 method. apparently it is popularized by elizabeth warren? the idea is you spend only 50% of your budget on needs, 30% on wants, and 20% on savings or debt reduction (after counting all minimum payments on your current debt as part of Needs).

So I know my bills take up more than one of my 2 paychecks a month. (I ignore the occasional third one for budgeting purposes till it rolls around, so I don’t overbudget for months that don’t have one.) So for curiosity’s sake, I broke down my entire budget into Needs, Wants, and Savings, then did percentage math at it.

For this purpose, you count your non-tax payroll deductions, like healthcare and 401(k) contributions, as part of your income and expenses, but you don’t count money that goes away as taxes. So the budget starts off with putting 401(k) contributions in Savings and healthcare deductions in Needs. Then you start listing off shit like rent, utilities, car expenses…

Right now, while I’m still catching up on a bunch of my COVID-deferred bills and loans, my Needs come out to about 74% of my income. However, my Wants are very minimal: I have my massage subscription and tip, I’ve budgeted for fast food or takeout maybe 2-3x a month, and I pledge to one Patreon at the $1 level. All together, my Wants are about 6% of my income, leaving the requisite 20% to go toward reducing COVID debt for now.

However, once my COVID deferrals are all paid off, my Needs go down to about 67% of my income – and this is with generous projections, like at least one specialist copay every single month and gasoline if we ever start driving again. My Wants stay at about 6%. So I could either use the other 27% for savings and debt reduction, or I could stick with the recommended 20% and have 13% of my budget for Wants.

And I’m like… this is so much money. This is $150 just unallocated *after* going out to eat at least once a month and keeping my massage subscription. That’s… I do not know what else I would want. I could buy my entire wardrobe at LL Bean. I could have a massage every single week. I could eat at a sit-down restaurant every week. I could buy the newest and most expensive iPhone every single year. I could buy a brand new American Girl doll every month with money to spare. Like I couldn’t do all of those at *once* obviously, but that’s with just 7% of my income by this method of reckoning.

Like, if I somehow did make twice my Needs expenses after tax. That’s not impossible; I’d have to make a little under $33k a year, or a little over $2700 a month, which would be about $17 an hour excluding taxes. I don’t expect to get there at my current job in the near future, but it’s not astronomical.

But like, at that point I’d be saving about $545 a month, covering all my Needs expenses, and I would have *over eight hundred dollars a fucking month* to spend on Wants! Like… jesus fuckwaffles. How would I… I could buy a new one of my current phone every single month and have money left over. I could go to one of those black-tie restaurants that are like $100 a plate *twice a week*. I could not only move into a bigger apartment but hire a maid service to clean it. I could buy every single book I’ve ever read in short order and pay to store them all. I could live on like… caviar and avocado toast.

Hell, even if my living expenses were somehow miraculously reduced and my Needs were only half of my tax-excluded pay *now*, I’d be living on a little over $1000 a month, saving about $400 a month, and trying to figure out how to spend $600 a month on Wants. How… I don’t fucking know what else I could want. I’m not used to having money to spare. It’s weirder than winning the lottery, even, because it’s just like… it’s not enough to go “I will pay off all my friends’ student loans and buy a condo!” but it’s enough that I’m like “Do I just… put all 27% of my income in savings? Do I save for a car? Pay off my student loans? Invest for retirement? Am I fundamentally missing something I should be wanting?”

That sounds like a sign that 50/30/20 isn’t for you.

A lot of budgeting methods have this…maybe not “problem” exactly, but this thing where they’re clearly aimed at people who start with an entertainment budget of “everything after necessities” (or in many cases even higher) and negotiate *downwards*, which makes the methods a bad fit for people who start with an entertainment budget of zero and negotiate *upwards*. I guess the people spending money they don’t have on things they could do without are the ones most in need of frameworks, so the frameworks are designed for them. Getting *down* to 30% is a good start for people who were previously spending *more*.

—

Personally, I do struggle to wrap my head around things that draw a bright line between “wants” and “investments”. Sure, there are *occasional* items–like restaurant food–that are just wants and not also investments, but by far the most common reason for me to want to buy something is because I think it will leave me better off in the long run. I have a long list of things to save up for, and it’s all stuff like “house repairs” and “things that give you a leg up on Vimes Boot Theory” and “retirement funds” and “hedging against the future being wildly different from the present, such that normal retirement funds don’t cut it [link]”.

—

I think it’s important to bear in mind: given how weird your life is in general, and in particular the fact that your ability to work has a history of fluctuating erratically, saving is even more important for you than for most people.

There’s a concept called “self-insurance”. (…actually it turns out that there are at least *two* similar-but-not-identical concepts called self-insurance, and the Wikipedia article is about the wrong one. Investopedia [link] has the right idea.) You, in particular, *really* should get disability insurance if you can possibly manage it, and while third-party disability-insurance companies *exist*, you’d have to file claims (during the periods of time when you are least capable of filing claims!), and take the risk that whatever shit happens to you next won’t technically be disability by their standards, and operate under rules designed to let the insurance company turn a profit. (The house always wins.) Ideally, then, what you’d want is to instead save up enough in the good times that you can cover the bad times yourself.

(For example: you mention you’re digging your way out of COVID-related debt. My brother was temporarily laid off in the spring, and because of [glitches in the hastily-expanded Canadian welfare system] was unable to receive any kind of unemployment payments in time to actually help him with it. But he had lots of money in his savings account, and he used some of *that* to cover his bills until the restaurant re-opened. Now that he’s working again, he’s replenishing it; in the long run, he plans to save up enough for a condo.

(We not-quite-joked that if the glitch had to happen to *someone* at his workplace, it’s good that it happened to him: his co-workers spend all their money on booze and weed and wouldn’t have been able to handle it. His co-workers, meanwhile, not-quite-joke that they should get him hooked on something so they can drag him back into the crab bucket.))

Yeah, idk if I’m just not looking in the right places, but the budgeting advice I can find all seems to skew really strongly toward “quit your starbucks habit! cut off the cable channels you don’t watch! do you really need a cell phone?” rather than like… you know, “I was raised on 3¢ a chore, I have absolutely no idea how financially healthy people cope with having discretionary income and I want guidelines”.

—

My priorities are different from yours obviously, but yeah, my list of things to save up for (other than straight-up debt reduction, which is a big one) are things like “new orthotic shoes” and “when my car breaks down again”. Freedom, essentially. Transportation is big for me, even though my current place of residence has by far the best public transit system I’ve used outside of Washington DC. (Buses every 10-15 minutes? Wtf is this sorcery?) Maybe moving into a ground-floor apartment eventually so I can stop carrying groceries up the fucking stairs, but I’d have to afford to pay movers because I can’t physically get my loveseat down the stairs by myself. And when it comes down to it, I kind of prefer not having to actually move everything.

—

I actually have disability insurance through my work, and then I managed to completely space on it while I was out on FMLA and didn’t realize I had it till I was back to work and scrutinizing my pay stubs – I thought I’d opted out of it last open enrollment. So I never got as far as finding out whether a depressive collapse counted as disability, or whether I could have filed a claim or anything. :P So yeah, with open enrollment just around the corner again, I am pondering whether to keep paying the approximately $15/paycheck toward disability insurance or not. I haven’t used my dental or vision insurance yet either but I keep meaning to… it’s just that for all I’ve lived here for over two years, I still don’t know things like “where is a good dentist”.

(My eyesight varies wildly with my diabetes. When my blood sugar is under control, I don’t seem to need glasses. When it’s out of control, I see so badly that I didn’t realize there were artificial cobwebs all over the call floor my first Halloween at this job and just thought my vision was inexplicably foggy in addition to being unfocused.)

—

I like the idea of having retirement income, and of employer matching, but yeah, the way my life tends to go, and especially with the way I burn out at irregular intervals, I’m honestly not sure when or whether the whole “tax-advantaged” thing (which I will freely admit I don’t actually understand) outweighs the benefits of cash on hand. Right now, my plans go approximately as follows:

* Catch up on car insurance payments before the new policy starts in November and stacks on top of my deferred balance.

* Pay the CPAP mask bill that went to collections like a year ago and I haven’t had the spoons or the money to get it out yet, also buy a new CPAP mask as this one is becoming elderly and I’m having to kludge it back together when the plastic pieces break.

* Pay off the cell phone deferral early just for the hell of it because I should have the money and it’ll drop my bill by $20/month. (I already finally got my employee discount applying so I’ll be down to like $35/month for unlimited data with no hotspot. God, the ability to *not* need hotspot is such a weird luxury…)

* Pay back @camshaft22 for loaning me like three months’ rent over the course of the pandemic. If all my budgeting is correct I might be able to do that by January.

* Assuming 2020 has not yet exploded in my face too disastrously, build up that emergency fund everyone talks about. This comes after the COVID debt because being able to sock away $400+ a month will be very encouraging for me at that point. Right now my savings is just, I’m manually doing the thing where you round up each purchase to the next dollar and put the change in savings. It’s… complicated, because my savings account takes several days to process a transfer from checking once I request it, so e.g. right now I have no less than five scheduled transfers, each under $1, requested as early as Thursday night, which are not going to process until Tuesday at the earliest because of Labor Day. Once I get the car insurance paid up, which is the situation with a definite time pressure, I might start rounding up to the next $5 mark if I think I can afford it. I know in the olden days, just having each purchase rounded up to the next dollar could wind up bringing me like $26 in savings a month, but I think that’s when I was like buying snacks from the vending machine and stuff.

* Once I have an emergency fund, find out what the deal is with my credit cards in collections and pay them off. There’s one I would have sworn I paid but my credit reports all still show it derogatory.

* Then it’s a decision between “Save every possible penny for a car made in this millennium that has not been totaled, before my current car explodes irreparably” or “Try to get my student loans out of default while also saving at a slower rate for a car, so that if my car explodes before I can buy a new one out of pocket, I might have a hope in hell of getting a car loan that’s not completely horrendous”.

Of course, the downside of this is if my car explodes *before* I have an emergency fund, I’m in trouble. Again. :P October has that third paycheck though, so it’s really tempting to put the whole bloody thing toward debt reduction and knock some of these out of the park.

>>(Buses every 10-15 minutes? Wtf is this sorcery?)

*impressed whistle*

—

>>FMLA

*googles*

I was about to say “holy shit, why can’t *we* have something like that”, but then I looked closer and it has so many exceptions that for all I know we *do* have an analogous law, and I just haven’t noticed because it would never come up in real life. I’m glad you managed to actually get caught in that hole-ridden safety net.

Our 2019!unemployment-system, because it makes the employer pay extra into the system every time they allow you to go an entire week without work, has the emergent effect of *banning unpaid sick leave*. Well, you can have up to six days at a time of unpaid sick leave, but of course that’s not enough to get over a cold.

(I am very glad they scrapped the idea of returning to the 2019 system in September, because the 2019 system *encourages* the spread of disease and that is the *last* thing we fucking need right now. Meta-Boss has, at least twice, coerced me into returning to (customer-facing!) work while still having coughing fits† because he didn’t want to eat the fine for allowing me to become technically unemployed (even though I wouldn’t have bothered actually applying for unemployment, knowing I would be returning to work in another week or two): I often wonder how many cases of illness can be traced back to the existence of the Canadian unemployment system. Between that and how hard it is to get them to actually give you any money, I think we’d be better off with *nothing* than with the 2019 system, especially with an active plague but even with just (“”just”“) baseline colds and flus.)

—

>>I haven’t used my dental or vision insurance yet either but I keep meaning to… it’s just that for all I’ve lived here for over two years, I still don’t know things like “where is a good dentist”.

God, I’m so looking forward to having dental insurance††. I’ve been paying for vision checkups††† out of pocket because it’s just ~$150 every two years, but in theory dental is about that much every nine months. I haven’t had a dental checkup in two years, and the previous one was three years before that, and also I’m tired of every little toothache being like “is this it? is it happening? is today the day my wisdom teeth become an emergency?”.

(several of the things on the List are dental-related, and originally some of them were high enough in the priority order that we would have reached them by now, but we are postponing all non-urgent in-person medical care and *especially* stuff where you physically can’t wear a mask while you’re doing it)

And yeah, one of the many benefits of a stable housing situation is that I’ve long since found local medical providers I like. Now it’s just a matter of being able to afford the money and disease-risk to go see them.

—

>>I’m honestly not sure when or whether the whole “tax-advantaged” thing (which I will freely admit I don’t actually understand) outweighs the benefits of cash on hand.

Might be good for you to talk that over with an American finance nerd. I could talk your ear off about Canadian investment accounts, but the American situation is not perfectly analogous.

(Definitely look into what the early-withdrawal penalties are for various account types. One of the Canadian ones has almost no withdrawal penalty (there’s no fine, and you only have to wait until next year before you can put it back), to the point that it’s very feasible to put money into it knowing you’re going to need it again. (*I’m* not allowed to have that one, because the United States government hates me and wants me to suffer, but it *exists*.))

—

>>Then it’s a decision between “Save every possible penny for a car made in this millennium that has not been totaled, before my current car explodes irreparably” or “Try to get my student loans out of default while also saving at a slower rate for a car, so that if my car explodes before I can buy a new one out of pocket, I might have a hope in hell of getting a car loan that’s not completely horrendous”.

Yeah, cars are tough. Car loans are Not Done in my family, but we’re torn between “spend ~$6k on a *somewhat* less shitty car to tide us over until I start working full-time and can afford something better” and “jump straight to the ~$14k hybrid we really should have in the medium term (while we wait for full-electric hatchbacks to [be remotely affordable + have a range capable of New York trips]: currently you can have at most one of those things)”. A 14k car would wipe out an uncomfortable amount of savings, but likely have *much* lower maintenance costs than a 6k.

(Of course, summer is ending (= broken air conditioner is ceasing to matter for another year) plus we’re still not driving much, so “keep using the beater until I start working full-time” might also be a workable option. But my parents occasionally make noises about maybe returning to delivery driving.)

—

†And of course masks were *also* forbidden back then, because in the Old Times they signalled (in this case correctly, but anyway) having a cold and the *appearance* of sanitation is far more important to Meta-Boss than actually *being* sanitary.

††not covered by government between the ages of 14 and 65, and maybe not rich children either

†††not covered by government between the ages of 20 and 65, unless you have a degenerative eye condition (diabetes counts!)

Tags:

#and because people are constantly opening the front door and letting in pollen #I used to get a lot of sore throats from the no-masks-allowed policy #I wasn’t confident that wearing a mask at work would be enough to stop it but now I know from experience #if I’m still working there after the vaccine #I’m gonna show up in a cloth mask with ”pollen mask” written on it and refuse to take it off #”it’s a disability accommodation” #”give me any paperwork you need me to fill out for that and I’ll fill it out‚ but I am not taking off this mask” #venting cw? #(the before-times Canadian unemployment system fills me with rage) #((for that matter the United States tax code also fills me with rage)) #((but y’all knew that one already)) #adventures in human capitalism #in which Brin has a job #illness tw #poison cw? #covid19 #reply via reblog #medical cw #our home and cherished land #home of the brave #allergies #long post

so like. there’s this budgeting thing called the 50/30/20 method. apparently it is popularized by elizabeth warren? the idea is you spend only 50% of your budget on needs, 30% on wants, and 20% on savings or debt reduction (after counting all minimum payments on your current debt as part of Needs).

So I know my bills take up more than one of my 2 paychecks a month. (I ignore the occasional third one for budgeting purposes till it rolls around, so I don’t overbudget for months that don’t have one.) So for curiosity’s sake, I broke down my entire budget into Needs, Wants, and Savings, then did percentage math at it.

For this purpose, you count your non-tax payroll deductions, like healthcare and 401(k) contributions, as part of your income and expenses, but you don’t count money that goes away as taxes. So the budget starts off with putting 401(k) contributions in Savings and healthcare deductions in Needs. Then you start listing off shit like rent, utilities, car expenses…

Right now, while I’m still catching up on a bunch of my COVID-deferred bills and loans, my Needs come out to about 74% of my income. However, my Wants are very minimal: I have my massage subscription and tip, I’ve budgeted for fast food or takeout maybe 2-3x a month, and I pledge to one Patreon at the $1 level. All together, my Wants are about 6% of my income, leaving the requisite 20% to go toward reducing COVID debt for now.

However, once my COVID deferrals are all paid off, my Needs go down to about 67% of my income – and this is with generous projections, like at least one specialist copay every single month and gasoline if we ever start driving again. My Wants stay at about 6%. So I could either use the other 27% for savings and debt reduction, or I could stick with the recommended 20% and have 13% of my budget for Wants.

And I’m like… this is so much money. This is $150 just unallocated *after* going out to eat at least once a month and keeping my massage subscription. That’s… I do not know what else I would want. I could buy my entire wardrobe at LL Bean. I could have a massage every single week. I could eat at a sit-down restaurant every week. I could buy the newest and most expensive iPhone every single year. I could buy a brand new American Girl doll every month with money to spare. Like I couldn’t do all of those at *once* obviously, but that’s with just 7% of my income by this method of reckoning.

Like, if I somehow did make twice my Needs expenses after tax. That’s not impossible; I’d have to make a little under $33k a year, or a little over $2700 a month, which would be about $17 an hour excluding taxes. I don’t expect to get there at my current job in the near future, but it’s not astronomical.

But like, at that point I’d be saving about $545 a month, covering all my Needs expenses, and I would have *over eight hundred dollars a fucking month* to spend on Wants! Like… jesus fuckwaffles. How would I… I could buy a new one of my current phone every single month and have money left over. I could go to one of those black-tie restaurants that are like $100 a plate *twice a week*. I could not only move into a bigger apartment but hire a maid service to clean it. I could buy every single book I’ve ever read in short order and pay to store them all. I could live on like… caviar and avocado toast.

Hell, even if my living expenses were somehow miraculously reduced and my Needs were only half of my tax-excluded pay *now*, I’d be living on a little over $1000 a month, saving about $400 a month, and trying to figure out how to spend $600 a month on Wants. How… I don’t fucking know what else I could want. I’m not used to having money to spare. It’s weirder than winning the lottery, even, because it’s just like… it’s not enough to go “I will pay off all my friends’ student loans and buy a condo!” but it’s enough that I’m like “Do I just… put all 27% of my income in savings? Do I save for a car? Pay off my student loans? Invest for retirement? Am I fundamentally missing something I should be wanting?”

That sounds like a sign that 50/30/20 isn’t for you.

A lot of budgeting methods have this…maybe not “problem” exactly, but this thing where they’re clearly aimed at people who start with an entertainment budget of “everything after necessities” (or in many cases even higher) and negotiate *downwards*, which makes the methods a bad fit for people who start with an entertainment budget of zero and negotiate *upwards*. I guess the people spending money they don’t have on things they could do without are the ones most in need of frameworks, so the frameworks are designed for them. Getting *down* to 30% is a good start for people who were previously spending *more*.

—

Personally, I do struggle to wrap my head around things that draw a bright line between “wants” and “investments”. Sure, there are *occasional* items–like restaurant food–that are just wants and not also investments, but by far the most common reason for me to want to buy something is because I think it will leave me better off in the long run. I have a long list of things to save up for, and it’s all stuff like “house repairs” and “things that give you a leg up on Vimes Boot Theory” and “retirement funds” and “hedging against the future being wildly different from the present, such that normal retirement funds don’t cut it [link]”.

—

I think it’s important to bear in mind: given how weird your life is in general, and in particular the fact that your ability to work has a history of fluctuating erratically, saving is even more important for you than for most people.

There’s a concept called “self-insurance”. (…actually it turns out that there are at least *two* similar-but-not-identical concepts called self-insurance, and the Wikipedia article is about the wrong one. Investopedia [link] has the right idea.) You, in particular, *really* should get disability insurance if you can possibly manage it, and while third-party disability-insurance companies *exist*, you’d have to file claims (during the periods of time when you are least capable of filing claims!), and take the risk that whatever shit happens to you next won’t technically be disability by their standards, and operate under rules designed to let the insurance company turn a profit. (The house always wins.) Ideally, then, what you’d want is to instead save up enough in the good times that you can cover the bad times yourself.

(For example: you mention you’re digging your way out of COVID-related debt. My brother was temporarily laid off in the spring, and because of [glitches in the hastily-expanded Canadian welfare system] was unable to receive any kind of unemployment payments in time to actually help him with it. But he had lots of money in his savings account, and he used some of *that* to cover his bills until the restaurant re-opened. Now that he’s working again, he’s replenishing it; in the long run, he plans to save up enough for a condo.

(We not-quite-joked that if the glitch had to happen to *someone* at his workplace, it’s good that it happened to him: his co-workers spend all their money on booze and weed and wouldn’t have been able to handle it. His co-workers, meanwhile, not-quite-joke that they should get him hooked on something so they can drag him back into the crab bucket.))

Tags:

#reply via reblog #adventures in human capitalism #covid19 #illness mention #drugs cw #101 Uses for Infrastructureless Computers #is the blue I see the same as the blue you see

Been spending kinda-scary-when-I’m-not-sure-when-I’ll-make-money-again amounts of money on new house stuff because we need all sorts of things likes oven mitts and bleach and plungers, etc. It’s interesting to see how much stuff is out of stock on Amazon because of the pandemic, and I really wish I had visibility into what bottlenecks are responsible. Why is this kitchen stool available in red tend days from now, but indefinitely unavailable in black? Is it some dye shortage? Why is this hand mixer available with attachments X, but not Y? What happened? I want to know but I’m destined not to

Tags:

#yes this #covid19 #adventures in human capitalism #illness tw #this probably deserves some other warning tag but I am not sure what

I can’t trust any take on Disney from someone so clearly ignorant of what he’s talking about that he can say this with a straight face:

“That is because in normal times you must choose perhaps four or five big rides, each lasting mere minutes, and spend hours waiting in line to be admitted to each.”

Dude, just showing up at a major Disney ride and expecting to be seated is like just showing up at a fancy restaurant and expecting to be seated: in both cases *you are supposed to make a reservation*. When I went in the autumn of 2015, ride reservations (“FastPasses”) were quite flexible (one-hour usage window) and very often available on a same-day basis: while we *had* reservations months in advance, we made last-minute adjustments to them pretty much every day (you can do this on your phone, thanks to the complimentary Wi-Fi [link]).

(Also a part of me is going “you’re complaining about how expensive everything is and yet you stayed at the fucking *Contemporary*??”, while another part goes “why did the Atlantic send some poor dude with a COVID-19-naive immune system to fucking *Florida*? they’re a bunch of Americans in the summer of 2020: did they *seriously* not have anybody who’d had it already that they could send instead?”)

Still, it’s interesting to hear some reporting from the field. Just…with some caveats.

That is all relatively recent, though. Fastpass was introduced in 1999; I definitely remember the process he describes from when I was growing up. And the author is of course describing how Disney “usually” is off of secondhand reports, since he’s never been before.

But yeah, the article is great as a description of how Disney is now. And the observations about it as being part of the American civic religion aren’t original but they are fairly good points.

I *suppose* you could call 21 years relatively recent compared to the total span of Disney World’s existence, but it’s simultaneously a long time.

I guess a generational thing does add another layer to the bit about his parents refusing to go there: *I* grew up hearing Dad complain about “standing in line for hours for every five minutes of ride” as the reason he refused to go to *Six Flags*, and perhaps even specifically as a reason why Disney was better than Six Flags.

(A bit of context: I was born in 1993 to a family that *was* upper-middle-class at the time and a mom that loves Disney World. I’ve been five times: 1998, 2000, 2001 (we were there on 9/11, it was a hell of a thing), 2004, and 2015. Our trips were generally around 1.5 – 2 weeks long: trying to cram everything into a long weekend is a recipe for exhaustion and FOMO.)

—

In additional to the description of how things were going on the ground, I thought the bits about the Disney World government having legitimacy in the eyes of its constituents, in a way the American government does not, were an interesting way of looking at it.

Yeah, I think there’s something of a generational thing going on there maybe?

I was born 1986 and we went to Disney World like eight or ten times when I was a kid/teenager. I think we might have gone there, one way or another, every year from 95 or 96 to 2000 or 2001 or something like that? And then I wound up there again in 2004.

(And then I also went to Disneyland in August 2004 because it was effectively a compulsory part of college orientation, long story. I used my deep knowledge of Disney World to go around with a couple friends and maximize the time we could spend in air conditioning. I think we rode Small World multiple times becuase it was shady, air conditioned, and had short lines.)

Fastpass was introduced toward the end of that, so I definitely remember it as “that new thing they just rolled out that makes the lines easier to deal with”. But by the time they’d introduced it I was absolutely fucking sick of going to Disney World.

But yeah, if you asked me what Disney World was like, my gut reaction was “Standing in these awful lines constantly, although I think they did a thing to make that better recently.” Also, I don’t know how the system works now, but when Fastpass was new you could only have one at a time. So you’d get a Fastpass for a long-line ride like Space Mountain or something, and then you’d go stand in long lines for other attractions while you waited for your time to come around. So it let you do more things but still the dominant experience was “standing in line”.

But yeah, the bits about Disney’s “governmental” legitimacy were really interesting. I kept using the phrase “American Singapore” to a Disneyphile friend today, who eventually responded: “I think there’s a limit to my appreciation of the dystopian artwork in which we find ourselves.”

As of 2015, there were three tiers of ride and you started off with one reservation in each tier. There were circumstances (I’m not sure of the exact rules now) where you could snap up extra FastPasses that other people had abandoned (and/or perhaps that Disney had added upon seeing the ride wasn’t full enough), and I remember them being fairly easy to find. But OTOH this *was* September, a month so slow that Disney bribed us with a free meal plan to schedule our trip for that time period.

(Joke’s on them: we were planning to go for September anyway. That meal plan was great: more credits than we could possibly use (presumably it was aimed to accommodate people with much higher appetites), and with prices denoted simply in “meals” and “snacks” rather than dollars. Being 100% price-insensitive in your food-buying decisions is a wonderfully liberating experience.)

Tags:

#reply via reblog #Disney #politics cw #illness tw #covid19 #home of the brave #food #adventures in human capitalism #disordered eating?

Oh huh. when Horizon Zero Dawn PC came out it was very cheap, ZAR 236 (~USD 13), and I bought it quickly because I knew I wanted it and I assumed it was a mistake on steam’s part that I could take advantage of. They later tripled the price to ZAR 680 (~USD 40), which I thought was them fixing it.

Turns out what actually happened was that this was just steam’s regional pricing adjustment at work, but the adjustment was so steep (particularly in Argentina, which was only USD 7 equivalent) and for such a popular game that loads of people used VPN’s to buy the game at foreign pricing.

Lowering the effective price for other countries is a pretty sensible move on Steam’s part, and I hope they don’t stop doing it. The South African Rand is nowhere near the weakest currencies out there, but the amount of disposable income here is much lower (heck, South Africa only /got/ a legal minimum wage last year, and it’s about USD 1.3/hour after a 10% hike this year) and paying dollar prices is hells of expensive. 60 dollars is pricey in the USA, but paying ZAR 1000 in South Africa is hideously expensive for many people. It’s even worse in places like Kenya or Indonesia. There’s a reason why I’m considering moving my server infrastructure to Russian providers who work in Rubles.

dang that’s a low minimum wage. what’s rent / general expenses like

Big Mac index is about 50%, i.e. you pay half as much for a big mac here than in the USA in raw currency terms, and that calculation more or less carries to a lot of food products, cost of living and so on. As you can imagine, ½ USA expenses but ⅙th USA minimum wage means living on minimum wage Is Not Great.

If you work 40 hour weeks at minimum wage you make ~ZAR 3300 (USD 200), and the lowest rent 1 bedroom apartment you can get anywhere near a city is usually around ZAR 2000. Rural areas are cheaper but there’s actually an adjustment on minimum wage for farm workers that drops it to like ZAR 18 per hour, or about One Dollar. You can make up to 3-4× minimum wage without a degree in most cases if you manage to work up to like, store manager or whatever, but that’s kind of your cap without some kind of professional training. Food and other expenses eat the remaining money extremely fast.

If you’re on minimum wage and on your own it’s extremely hard to get by, and even with roommates or family it’s very rough, if you want to try renting. A lot of people live in multigenerational homes for historic, cultural and economic reasons. What “if you want to try renting” means is something I’ll get to under the cut, because unfortunately for this explanation, South Africa is less one economy as much as it is like three in a trench coat. We’ve already covered Low Income, but there’s also The Professional Class and Informal Economies.

can’t believe paypal continues to be like it is. how is this not considered fraudulent

anyway paypal is fine if you want to send another american us dollars, but you should more or less never accept payment through paypal. you will regret it

paypal is extremely opaque about the fees that it charges. and once they’ve charged a fee, there’s more or less no way to undo it. if you immediately ‘refund’ such a transaction, it actually means you’re giving back the money you received *and* paying the fee paypal charged.

they have two payment options – one of which is free and offers no ‘protection’ and the other of which is not and offers their ‘purchase protection’. you can instruct someone to send via the free option but there’s no guarantee they’re going to listen, or that they’re going to parse the options correctly even if they do, at which point there’s already money down the drain in the form of a fee and it’s just a question of who eats it.

this is what the page to pick looks like (gotta love that mobile first design):

here it says you might be eligible for purchase protection, and the ‘seller’ is going to pay a fee, but it doesn’t really explain what any of that means, or how much it will be.

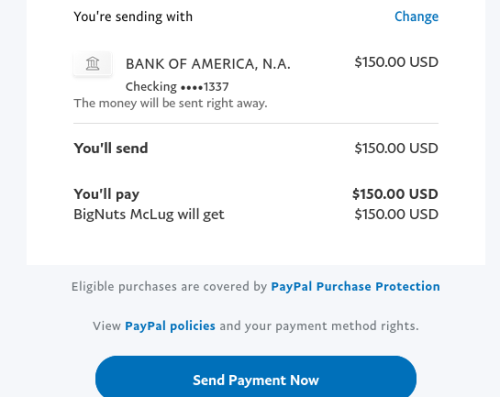

this is bad, because a lot of people will decide they might as well be protected, right? since it’s free. but the program is relatively picky and a lot of the times people use it it does not actually apply. but it gets worse. let’s say I’m sending $150 by paypal to my business partner:

it says right there BigNuts is going to get $150. he’s not. maybe in paypal’s accounting he gets the full amount and then pays the fee, but in practice he is never going to see the full amount. if Mr. McLug is in the US, he’s going to lose $4.35 on this.

but it gets worse if he’s international, as the fee gets jacked up – he’s going to lose $6.60 plus some change in whatever currency it’s going into. and the messaging gets much more confusing!

paypal still pretends there’s no fee for a goods & services transaction, but if you send via the lower cost option, it shows you the currency conversion charge up front.

if you’re sending $1000, the currency conversion charge is $5. if you’re sending goods and services, it’s $44 but to the sender it looks like $0.

so paypal is basically conning people into creating these fees in exchange for what is often a nonexistent guarantee. ok, what else?

well, paypal tries to bill itself as a ‘safe’ way to receive money over the internet, but it’s not actually better than anything else. it’s still part of the financial system.

if someone pays you via paypal, you still need to do all the work of verifying that they’re a real person and not scamming you, because there is no protection. if the payment paypal received gets revoked or marked as fraudulent, guess who’s covering it. you!

this is a pretty common move for scammers, because I guess people trust paypal and think they can actually trust payments they receive by it. but if you want to take money from someone you don’t trust, you basically need to do cash or bitcoin or something like that.

now, payment processors are famous for this sort of shit. and if you’re a merchant, you might write it off as the cost of doing business. the frauds will be amortized to an acceptable cost over your whole volume of transactions.

but if you’re just some person doing a one off transaction, this is much less true. and paypal makes this deliberately more confusing instead of being transparent.

This, and also:

Did you know there’s an arms race going on between [Canadian freelancers who get paid in USD] and Paypal, where Canadians try to withdraw into USD-denominated bank accounts (to avoid Paypal’s terrible exchange rates, and perhaps use the USD directly) and Paypal tries to stop them?

Last I heard, Paypal was winning. (edit: apparently the Canadians have struck back, but the method they’re using these days costs $4/month, so even if you can get it working it’s only worth it for sufficiently high volumes. [link])

—

(And God help you if you want to *send* an American money: even if you have the USD lying around because you weren’t allowed to withdraw it at a reasonable exchange rate, a USD$3 flat fee is huge when you’re only dealing with a few dollars at a time.)

Tags:

#adventures in human capitalism #reply via reblog #PSA #our home and cherished land #home of the brave